Can Quality Screens Reduce Small-Cap Balance-Sheet Risk? Russell 2000 Test in Python

June 12, 2026

What's the question?

Small-cap investing often mixes two different exposures: size and financial fragility. A small company can be cheap because it is overlooked, or because it has weak profitability, thin cash generation, and too much debt. A quality screen attempts to separate those cases.

The question is whether a simple quality score can identify materially stronger balance-sheet profiles inside a point-in-time Russell 2000 sample. The goal is not to forecast returns. The goal is to reduce avoidable balance-sheet risk before doing deeper security analysis.

The approach

The analysis uses 300 Russell 2000 constituents as of December 31, 2025. Built from SEC EDGAR public filings and market data, it then pulls the latest annual metrics for those companies.

- Pull point-in-time Russell 2000 constituents with

as_of="2025-12-31" - Pull ROE, free-cash-flow margin, debt/assets, interest coverage, and market cap

- Remove records with missing data and extreme pre-revenue or distressed accounting values

- Winsorize the scoring inputs at the 5th and 95th percentiles

- Reward higher ROE, higher free-cash-flow margin, lower leverage, and higher interest coverage

The outlier controls are part of the method. Without them, a few extreme small-cap observations dominate the score.

Code

import xfinlink as xfl

import pandas as pd

xfl.set_api_key("YOUR_API_KEY") # free at https://xfinlink.com/signup

members = xfl.index("russell2000", as_of="2025-12-31", limit=300)

tickers = members["ticker"].dropna().tolist()

fields = ["roe", "fcf_margin", "debt_to_assets", "interest_coverage", "market_cap"]

df = xfl.metrics(tickers, period_type="annual", period="3y", fields=fields)

latest = df.sort_values("period_end").groupby("ticker").tail(1).set_index("ticker")

screen = latest[fields].dropna()

screen = screen[

screen["roe"].between(-1, 1)

& screen["fcf_margin"].between(-1, 1)

& screen["debt_to_assets"].between(0, 1.5)

]

print(screen[["roe", "fcf_margin", "debt_to_assets"]].describe())Full script with formatting and visualisation: russell2000-quality-balance-sheet-python.py

Output

=== Russell 2000 Quality Balance-Sheet Screen ===

Membership date: 2025-12-31

Constituents requested: 300

Complete annual metric records: 176

Records after outlier controls: 129

Top quality quintile median ROE: 12.7%

Bottom quality quintile median ROE: -14.1%

Top quality quintile median debt/assets: 5.0%

Bottom quality quintile median debt/assets: 40.1%

Top quality names:

TBBK score= 7.17 ROE= 33.1% FCF_margin= 36.6% debt/assets= 2.3% interest_cover= 298.1 market_cap=$2,393M

AII score= 7.10 ROE= 29.6% FCF_margin= 48.2% debt/assets= 0.0% interest_cover= 3385.0 market_cap=$330M

BANF score= 5.94 ROE= 13.0% FCF_margin= 34.3% debt/assets= 0.1% interest_cover= 75.0 market_cap=$3,828M

SRCE score= 5.65 ROE= 12.4% FCF_margin= 49.1% debt/assets= 2.6% interest_cover= 46.6 market_cap=$1,894M

APAM score= 5.31 ROE= 66.2% FCF_margin= 14.3% debt/assets= 12.0% interest_cover= 51.2 market_cap=$2,863M

AMTB score= 5.13 ROE= 5.6% FCF_margin= 29.4% debt/assets= 0.0% interest_cover= 5512.8 market_cap=$966M

AGYS score= 5.01 ROE= 11.9% FCF_margin= 21.3% debt/assets= 0.0% interest_cover= 87.3 market_cap=$2,585M

BWFG score= 4.99 ROE= 11.7% FCF_margin= 25.0% debt/assets= 5.4% interest_cover= 198.1 market_cap=$436M

Lowest quality names:

BKSY score= -6.25 ROE= -74.1% FCF_margin= -41.8% debt/assets= 52.1% interest_cover= -3.1 market_cap=$1,292M

BHR score= -4.80 ROE= -16.1% FCF_margin= -5.3% debt/assets= 119.1% interest_cover= 0.7 market_cap=$173M

BBAI score= -4.72 ROE= -48.0% FCF_margin= -33.3% debt/assets= 12.0% interest_cover= -11.8 market_cap=$1,809M

ARDX score= -4.70 ROE= -36.9% FCF_margin= -10.8% debt/assets= 40.4% interest_cover= -2.0 market_cap=$1,415M

TKNO score= -4.42 ROE= -25.1% FCF_margin= -24.2% debt/assets= 12.9% interest_cover= -77.2 market_cap=$236M

ADPT score= -4.40 ROE= -27.2% FCF_margin= -17.7% debt/assets= 24.7% interest_cover= -4.8 market_cap=$2,880M

BALY score= -4.37 ROE= -65.4% FCF_margin= -7.3% debt/assets= 39.7% interest_cover= -0.7 market_cap=$719M

BORR score= -3.93 ROE= 8.3% FCF_margin= -32.9% debt/assets= 61.8% interest_cover= 1.8 market_cap=$1,141MWhat this tells us

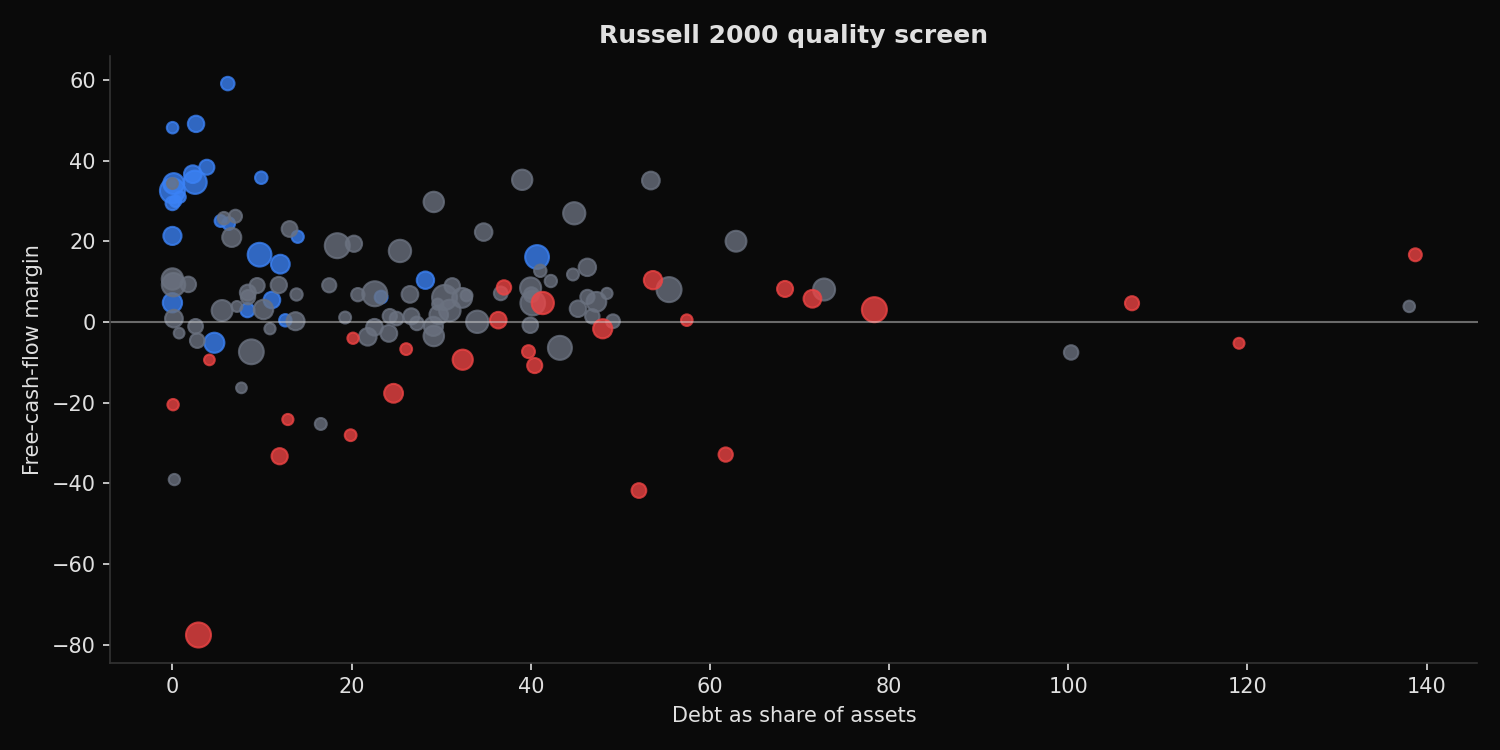

The screen separates the balance-sheet profile clearly. The top quality quintile has median ROE of 12.7% and median debt/assets of 5.0%. The bottom quality quintile has median ROE of -14.1% and median debt/assets of 40.1%.

That difference is economically meaningful. The top group is not merely less leveraged. It is also more profitable and more cash generative. The bottom group contains companies with negative free-cash-flow margins, weak interest coverage, and high balance-sheet pressure.

The outlier controls matter. Small-cap universes include early-stage companies, distressed companies, and accounting edge cases. A quality process should identify those cases explicitly rather than letting them dominate the score.

So what?

A Russell 2000 allocation can carry more balance-sheet risk than the index label suggests. Screening for quality before valuation helps avoid companies where cheapness may reflect financial fragility.

The practical use is as a triage step. Start with point-in-time membership, remove incomplete and distorted records, then rank profitability, free cash flow, leverage, and interest coverage. The result is a cleaner research queue for small-cap portfolios.

Built with xfinlink — free financial data API for Python. pip install -U xfinlink

pip install -U xfinlink