Does the Corporate Credit Spread Predict Stock Market Crashes? BAA-AAA Spread Analysis in Python

May 19, 2026

What’s the question?

Corporate credit spreads — the difference in yield between lower-quality (BAA) and higher-quality (AAA) bonds — reflect the market’s assessment of default risk. When spreads widen, the bond market is pricing in greater probability of corporate distress. If the bond market leads the equity market, widening spreads should predict larger subsequent stock market drawdowns. This has direct implications for risk management: credit spreads could serve as an early warning system.

The approach

Pull BAA and AAA yields from FRED (Moody’s seasoned corporate bond yields), SPY from xfinlink. 10 years of data. Compute spread z-score (252-day rolling), forward 3-month max drawdown, sort into quintiles.

import xfinlink as xfl

import pandas as pd

import numpy as np

from fredapi import Fred

xfl.api_key = "YOUR_API_KEY" # free at https://xfinlink.com/signup

fred = Fred(api_key=os.environ["FRED_API_KEY"])

# Credit spreads from FRED

baa = fred.get_series("BAA", observation_start="2016-01-01").rename("baa")

aaa = fred.get_series("AAA", observation_start="2016-01-01").rename("aaa")

spreads = pd.concat([baa, aaa], axis=1).dropna()

spreads["spread"] = spreads["baa"] - spreads["aaa"]

# SPY prices

spy = xfl.prices("SPY", start="2016-01-01", fields=["close"])

spy["date"] = pd.to_datetime(spy["date"])

spy = spy.set_index("date")["close"]

# Merge and compute z-score

merged = pd.concat([spreads["spread"], spy], axis=1).ffill().dropna()

merged["z"] = (merged["spread"] - merged["spread"].rolling(252).mean()) / merged["spread"].rolling(252).std()

# Forward 3-month max drawdown

fwd_dd = []

close_vals = merged["close"].values

for i in range(len(close_vals)):

if i + 63 < len(close_vals):

window = close_vals[i : i + 63]

fwd_dd.append(window.min() / window[0] - 1)

else:

fwd_dd.append(np.nan)

merged["fwd_dd"] = fwd_dd

analysis = merged.dropna(subset=["z", "fwd_dd"]).copy()

analysis["quintile"] = pd.qcut(analysis["z"], 5, labels=["Q1 (Tight)", "Q2", "Q3", "Q4", "Q5 (Wide)"])

print(analysis.groupby("quintile")["fwd_dd"].agg(["mean", "median", "count"]))Full script with formatting and visualisation: credit-spread-drawdown-signal-python.py

Output:

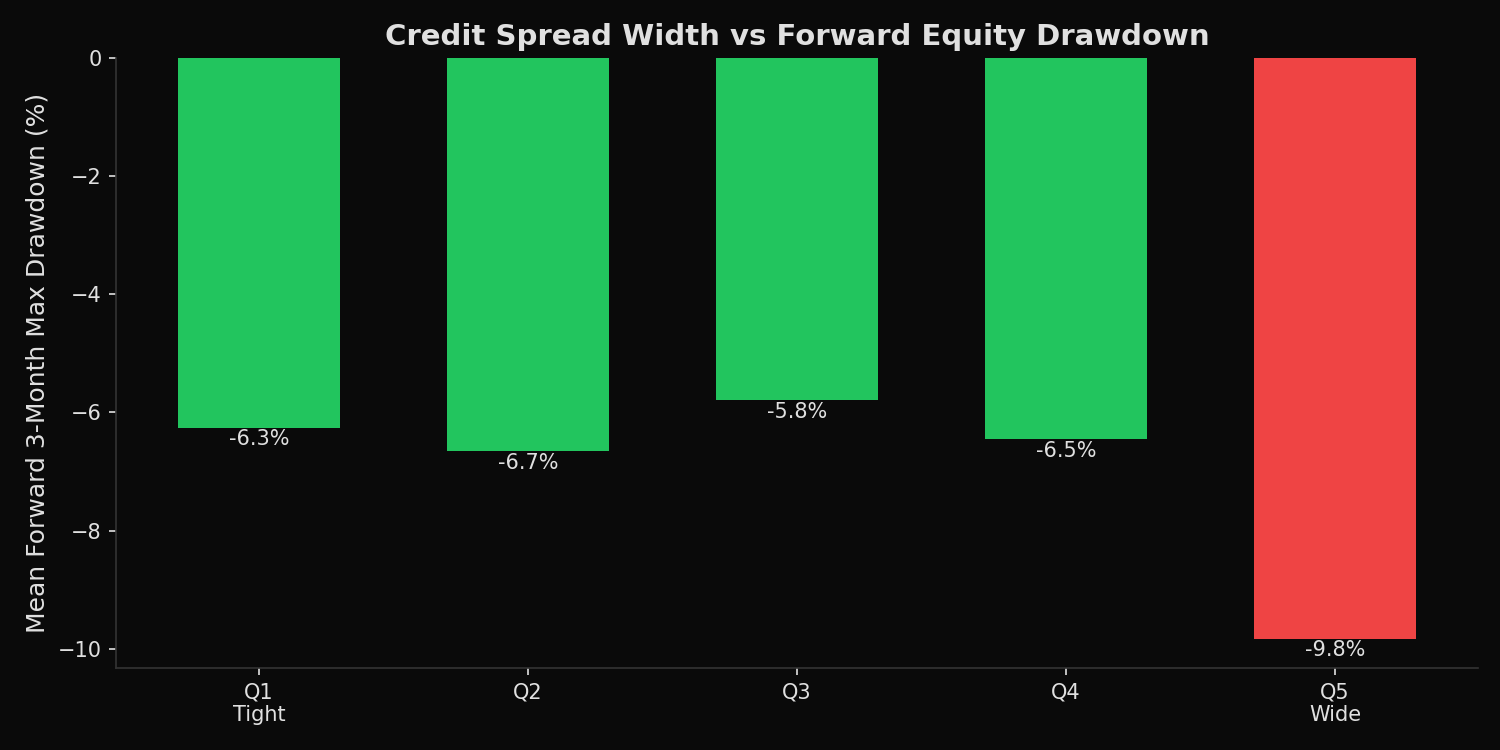

=== BAA-AAA Credit Spread vs Forward 3-Month SPY Max Drawdown ===

Q1 (Tight) mean_dd=-6.3% median_dd=-4.1% n=503

Q2 mean_dd=-6.7% median_dd=-4.1% n=503

Q3 mean_dd=-5.8% median_dd=-5.1% n=502

Q4 mean_dd=-6.5% median_dd=-6.6% n=503

Q5 (Wide) mean_dd=-9.8% median_dd=-9.1% n=503

Current spread: 0.61% z-score: -0.23What this tells us

The widest spread quintile (Q5) experiences forward 3-month drawdowns of -9.8% on average — 55% worse than the -6.3% for tight spreads (Q1). The median confirms this is not driven by outliers: Q5 median is -9.1% vs Q1 median of -4.1%. The relationship is monotonic in the tail — Q5 is distinctly worse than Q1-Q4, which cluster around -5.8% to -6.7%. The bond market does appear to lead equity risk, but only at extremes. Current spread z-score of -0.23 places the market in the benign Q2-Q3 range.

So what?

Monitor the BAA-AAA spread z-score as a risk overlay. When it exceeds +1.5 (well into Q5), tighten equity risk limits or increase cash allocation — the bond market is pricing in stress that equity markets have not yet reflected. Below +1.0, the signal is too noisy to be actionable. This is not a timing signal for entry or exit — it is a risk management signal for position sizing.

pip install xfinlink