Does the Oil-to-Gold Ratio Signal Recessions? XLE/GLD Backtest in Python

May 20, 2026

What’s the question?

Oil prices rise with economic activity. Gold prices rise with fear, uncertainty, and inflation hedging. The ratio of oil to gold (proxied by XLE/GLD) captures the market’s relative assessment of growth vs risk aversion. When the ratio falls sharply — oil underperforming gold — the market is pricing in weakening growth and rising risk premiums simultaneously. If this ratio carries forward-looking information, its rate of change should predict subsequent equity market performance.

The approach

10 years of XLE, GLD, and SPY. Compute the 12-month rate of change in XLE/GLD, sort into quintiles, measure mean forward 6-month SPY total return per quintile.

import xfinlink as xfl

import pandas as pd

import numpy as np

xfl.api_key = "YOUR_API_KEY" # free at https://xfinlink.com/signup

# 10 years of XLE, GLD, SPY

tickers = ["XLE", "GLD", "SPY"]

df = xfl.prices(tickers, start="2016-01-01", fields=["close"])

df["date"] = pd.to_datetime(df["date"])

# Pivot to wide format

wide = df.pivot_table(index="date", columns="ticker", values="close")

wide = wide.dropna()

# Compute XLE/GLD ratio and 12-month rate of change

wide["ratio"] = wide["XLE"] / wide["GLD"]

wide["ratio_roc_12m"] = wide["ratio"].pct_change(252)

# Forward 6-month SPY return

wide["fwd_6m"] = wide["SPY"].pct_change(126).shift(-126)

# Drop NaN and bin into quintiles

analysis = wide.dropna(subset=["ratio_roc_12m", "fwd_6m"]).copy()

analysis["quintile"] = pd.qcut(analysis["ratio_roc_12m"], 5,

labels=["Q1 (Falling)", "Q2", "Q3", "Q4", "Q5 (Rising)"])

print(f"Current XLE/GLD ratio: {wide['ratio'].iloc[-1]:.3f}")

print(f"12-month change: {wide['ratio_roc_12m'].iloc[-1]*100:+.1f}%\n")

for q in ["Q1 (Falling)", "Q2", "Q3", "Q4", "Q5 (Rising)"]:

sub = analysis[analysis["quintile"] == q]

print(f"{q:14s} fwd_ret={sub['fwd_6m'].mean()*100:+.1f}% n={len(sub)}")Full script with formatting and visualisation: oil-gold-ratio-recession-signal-python.py

Output:

Current XLE/GLD ratio: 0.139

12-month change: -47.5%

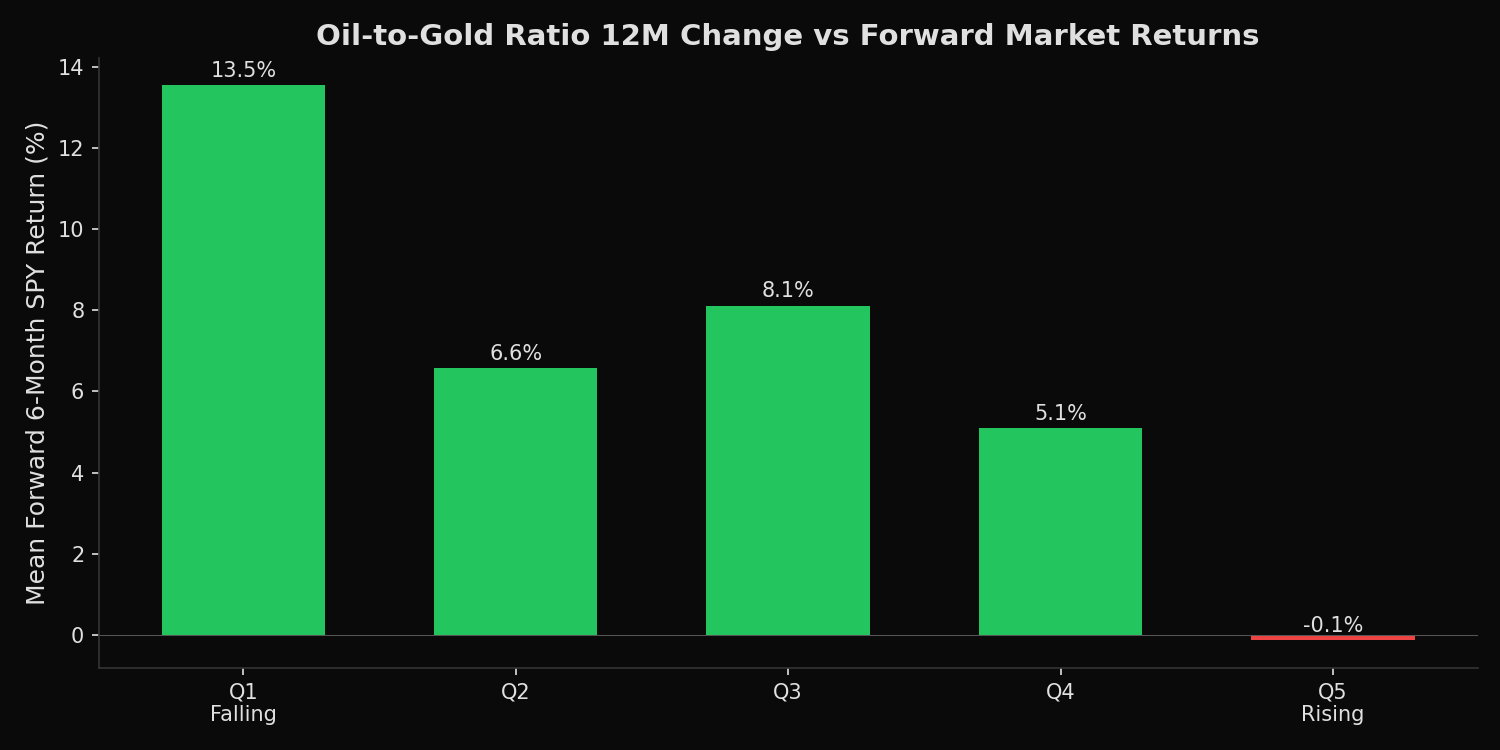

Q1 (Falling) fwd_ret=+13.5% n=444

Q2 fwd_ret=+6.6% n=444

Q3 fwd_ret=+8.1% n=443

Q4 fwd_ret=+5.1% n=444

Q5 (Rising) fwd_ret=-0.1% n=444What this tells us

The result is contrarian. When the oil-to-gold ratio is falling fastest (Q1) — indicating gold outperforming oil, a risk-off environment — forward 6-month SPY returns average +13.5%. This is the strongest quintile by far. When the ratio is rising fastest (Q5) — oil outperforming gold, a risk-on environment — forward returns are essentially zero (-0.1%). The interpretation: extreme risk-off conditions (falling ratio) tend to precede recoveries, while extreme risk-on conditions (rising ratio) tend to precede mean reversion. The current 12-month change of -47.5% places the market deep in Q1 territory.

So what?

The XLE/GLD ratio is a contrarian macro indicator, not a trend-following one. A sharply falling ratio (gold outperforming oil) historically precedes strong equity returns over the next 6 months. A sharply rising ratio historically precedes flat-to-negative returns. For tactical allocation, a 12-month decline exceeding -30% in the ratio is a historically favorable entry point for equities. A 12-month increase exceeding +30% is a signal to reduce risk.

pip install xfinlink