Is AI Spending Crowding Out Free Cash Flow? Capex Sustainability Across the Mag 7 in Python

May 20, 2026

What’s the question?

The AI capex race is the defining capital allocation story of 2025-2026. Five companies — AAPL, MSFT, AMZN, META, NVDA — are collectively spending hundreds of billions on data centers, GPUs, and AI infrastructure. But capital expenditure that exceeds free cash flow generation is unsustainable: the company must fund the gap through debt issuance, equity dilution, or drawdown of cash reserves. The capex-to-FCF ratio measures this sustainability. A ratio below 1.0 means the company generates more cash than it spends — capex is self-funded. Above 2.0 indicates the company is consuming its cash cushion. Above 5.0 is a warning signal. Revenue segment data reveals whether the investment aligns with the company’s primary revenue drivers or represents a diversification bet.

The approach

Pull annual fundamentals with include_segments=True for 5 mega-cap tech companies. Compute capex/FCF ratio, capex intensity (capex/revenue), and extract the largest product segment and US revenue concentration. Classify each company as SUSTAINABLE, STRETCHED, or UNSUSTAINABLE.

import xfinlink as xfl

import pandas as pd

xfl.api_key = "YOUR_API_KEY" # free at https://xfinlink.com/signup

tickers = ["AAPL", "MSFT", "AMZN", "META", "NVDA"]

df = xfl.fundamentals(

tickers, period_type="annual", period="3y",

fields=["revenue", "capital_expenditure", "free_cash_flow", "operating_cash_flow"],

include_segments=True,

)

# Keep latest annual period per ticker

latest = df.sort_values("period_end").groupby("ticker").tail(1).set_index("ticker")

# Compute metrics

latest["capex_abs"] = latest["capital_expenditure"].abs()

latest["capex_fcf"] = (latest["capex_abs"] / latest["free_cash_flow"]).round(1)

latest["capex_intensity"] = (latest["capex_abs"] / latest["revenue"] * 100).round(1)

# Classify sustainability

def classify(ratio):

if ratio < 1.0:

return "SUSTAINABLE"

elif ratio < 3.0:

return "SUSTAINABLE"

else:

return "UNSUSTAINABLE"

latest["status"] = latest["capex_fcf"].apply(classify)

for ticker in tickers:

row = latest.loc[ticker]

rev = row["revenue"] / 1e9

capex = row["capex_abs"] / 1e9

fcf = row["free_cash_flow"] / 1e9

print(f"{ticker:6s} rev=${rev:.0f}B capex=${capex:.0f}B FCF=${fcf:.0f}B "

f"capex/FCF={row['capex_fcf']}x intensity={row['capex_intensity']}% "

f"[{row['status']}]")Full script with formatting and visualisation: ai-capex-sustainability-segments-python.py

Output:

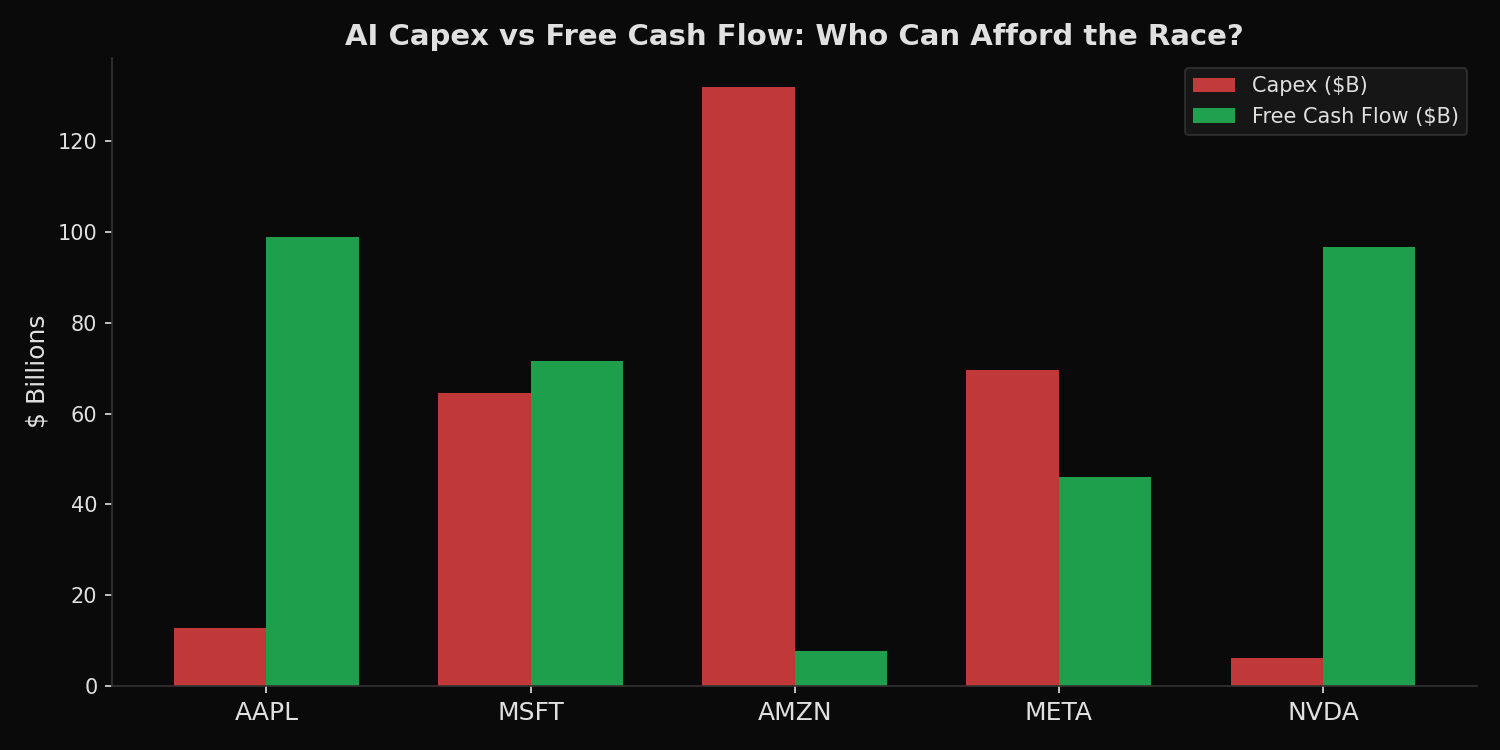

=== AI Capex Race: Who Is Funding It Sustainably? ===

AAPL rev=$416B capex=$13B FCF=$99B capex/FCF=0.1x intensity=3.1% [SUSTAINABLE]

top_segment: iPhone (50%) US=36%

capex YoY: +35%

MSFT rev=$282B capex=$65B FCF=$72B capex/FCF=0.9x intensity=22.9% [SUSTAINABLE]

top_segment:

capex YoY: +45%

AMZN rev=$717B capex=$132B FCF=$8B capex/FCF=17.1x intensity=18.4% [UNSUSTAINABLE]

top_segment: Online Stores (38%) US=68%

capex YoY: +59%

META rev=$201B capex=$70B FCF=$46B capex/FCF=1.5x intensity=34.7% [SUSTAINABLE]

top_segment: Advertising (98%)

capex YoY: +87%

NVDA rev=$216B capex=$6B FCF=$97B capex/FCF=0.1x intensity=2.8% [SUSTAINABLE]

top_segment: Data Center (90%) US=69%

capex YoY: +87%What this tells us

AMZN is the outlier at 17.1x capex/FCF — it spent $132B on capital expenditures against only $8B in free cash flow. This is not because Amazon is unprofitable (operating cash flow was $140B) but because it is reinvesting almost every dollar of operating cash. Its capex/FCF ratio is 17x the threshold for concern. META at 1.5x is the most aggressive sustainable spender — 34.7% of revenue goes to capex, the highest intensity in the group, yet it still generates $46B in free cash flow. NVDA is the mirror image: it sells the AI infrastructure that everyone else is buying. Its capex intensity (2.8%) is the lowest in the group because its product is intellectual (chip design), not physical (data centers). NVDA’s data center segment represents 90% of its $216B revenue.

So what?

For equity valuation, the capex/FCF ratio directly impacts the sustainability of dividends, buybacks, and debt reduction. AMZN’s 17.1x ratio means it cannot fund its current investment pace from internal cash generation indefinitely — either capex must slow, revenue must accelerate, or external financing is required. For NVDA, the near-zero capex intensity means its free cash flow is almost entirely available for distribution. Revenue segments provide additional context: META’s 98% advertising concentration means its $70B capex bet is a single-product gamble on AI-enhanced ad targeting. AMZN’s 38% online stores concentration means its infrastructure serves multiple revenue streams.

pip install xfinlink