Do Weak Jobs Reports Predict Market Drawdowns? NFP Surprise Event Study in Python

July 10, 2026

What's the question?

Non-Farm Payrolls (NFP) is the headline number from the US Bureau of Labor Statistics' monthly Employment Situation report. It counts the net change in paid employees across the US economy, excluding farm workers, government employees, private household workers, and nonprofit staff. The report is released on the first Friday of each month and is one of the most closely watched economic indicators in financial markets.

When the NFP number comes in well below expectations, the interpretation is that the labor market is weakening. A weakening labor market reduces consumer spending, lowers corporate revenue expectations, and raises the probability of recession. In June 2026, the US economy added only 57,000 jobs, well below consensus expectations. Unemployment fell to 4.2%, but only because 720,000 people left the labor force entirely. The natural question is whether historically weak NFP prints predict negative forward equity returns.

The alternative hypothesis is that weak NFP reports trigger a "Fed put" response: investors anticipate that the Federal Reserve will ease monetary policy to support the economy, and equity prices rise on rate cut expectations. Under this view, bad economic news is good news for stocks.

This analysis tests which interpretation the data supports. It examines 7 historically weak NFP releases between 2016 and 2026 and measures SPY forward returns over 5-day, 10-day, and 21-day horizons.

The approach

- Pull 11 years of daily closing prices for SPY to cover all NFP miss events

- Define 8 historically weak NFP report dates where the payroll number came in significantly below consensus expectations: May 2016 (38K), February 2019 (20K revision), September 2019 (130K), December 2020 (-140K), September 2021 (194K vs 750K expected), July 2024 (114K), October 2024 (12K, hurricane-impacted), and July 2026 (57K)

- For each date, compute the forward 5-day, 10-day, and 21-day return on SPY from the close on the report date

- Compare the average post-miss forward returns to the unconditional average forward returns over the full sample

- Run a one-sample t-test to determine whether the difference is statistically significant

The unconditional average serves as the benchmark. If weak NFP reports carry no information, post-miss returns should look similar to the full-sample average. If they carry predictive content, the means will diverge and the t-statistic will indicate significance.

Code

import xfinlink as xfl

import pandas as pd

import numpy as np

from scipy import stats

xfl.set_api_key("YOUR_API_KEY") # free at https://xfinlink.com/signup

df = xfl.prices("SPY", period="11y", fields=["close"])

df = df.sort_values("date").reset_index(drop=True)

nfp_miss_dates = pd.to_datetime([

"2016-05-06", "2019-02-01", "2019-09-06", "2020-12-04",

"2021-09-03", "2024-07-05", "2024-10-04", "2026-07-03",

])

windows = [5, 10, 21]

results = []

for nfp_date in nfp_miss_dates:

mask = df["date"] >= nfp_date

if not mask.any():

continue

td = df.loc[mask, "date"].iloc[0]

idx = df[df["date"] == td].index[0]

row = {"nfp_date": nfp_date, "trade_date": td}

for w in windows:

if idx + w < len(df):

row[f"fwd_{w}d"] = df.loc[idx + w, "close"] / df.loc[idx, "close"] - 1

else:

row[f"fwd_{w}d"] = np.nan

results.append(row)

event_df = pd.DataFrame(results)

uncond = {}

for w in windows:

uncond[f"fwd_{w}d"] = (df["close"].shift(-w) / df["close"] - 1).dropna().mean()

for _, r in event_df.iterrows():

f5 = f"{r['fwd_5d']:.2%}" if pd.notna(r['fwd_5d']) else "N/A"

f10 = f"{r['fwd_10d']:.2%}" if pd.notna(r['fwd_10d']) else "N/A"

f21 = f"{r['fwd_21d']:.2%}" if pd.notna(r['fwd_21d']) else "N/A"

print(f"{r['nfp_date'].strftime('%Y-%m-%d')} {f5:>8} {f10:>8} {f21:>8}")

for w in windows:

sample = event_df[f"fwd_{w}d"].dropna()

t_stat, p_val = stats.ttest_1samp(sample, uncond[f"fwd_{w}d"])

print(f" {w}-day: t={t_stat:+.3f}, p={p_val:.4f} n={len(sample)}")Full script with formatting and visualisation: weak-nfp-market-drawdown-signal-python.py

Output

FORWARD SPY RETURNS AFTER WEAK NFP REPORTS

NFP Date Trade Date 5-Day 10-Day 21-Day

--------------------------------------------------------------

2016-05-06 2016-05-06 -0.47% -0.11% 2.90%

2019-02-01 2019-02-01 0.15% 2.71% 3.32%

2019-09-06 2019-09-06 1.02% 0.08% -1.67%

2020-12-04 2020-12-04 -0.96% -0.18% 1.00%

2021-09-03 2021-09-03 -1.43% -4.20% -4.41%

2024-07-05 2024-07-05 0.96% -1.02% -6.72%

2024-10-04 2024-10-04 1.15% 2.03% -0.55%

2026-07-03 2026-07-06 N/A N/A N/A

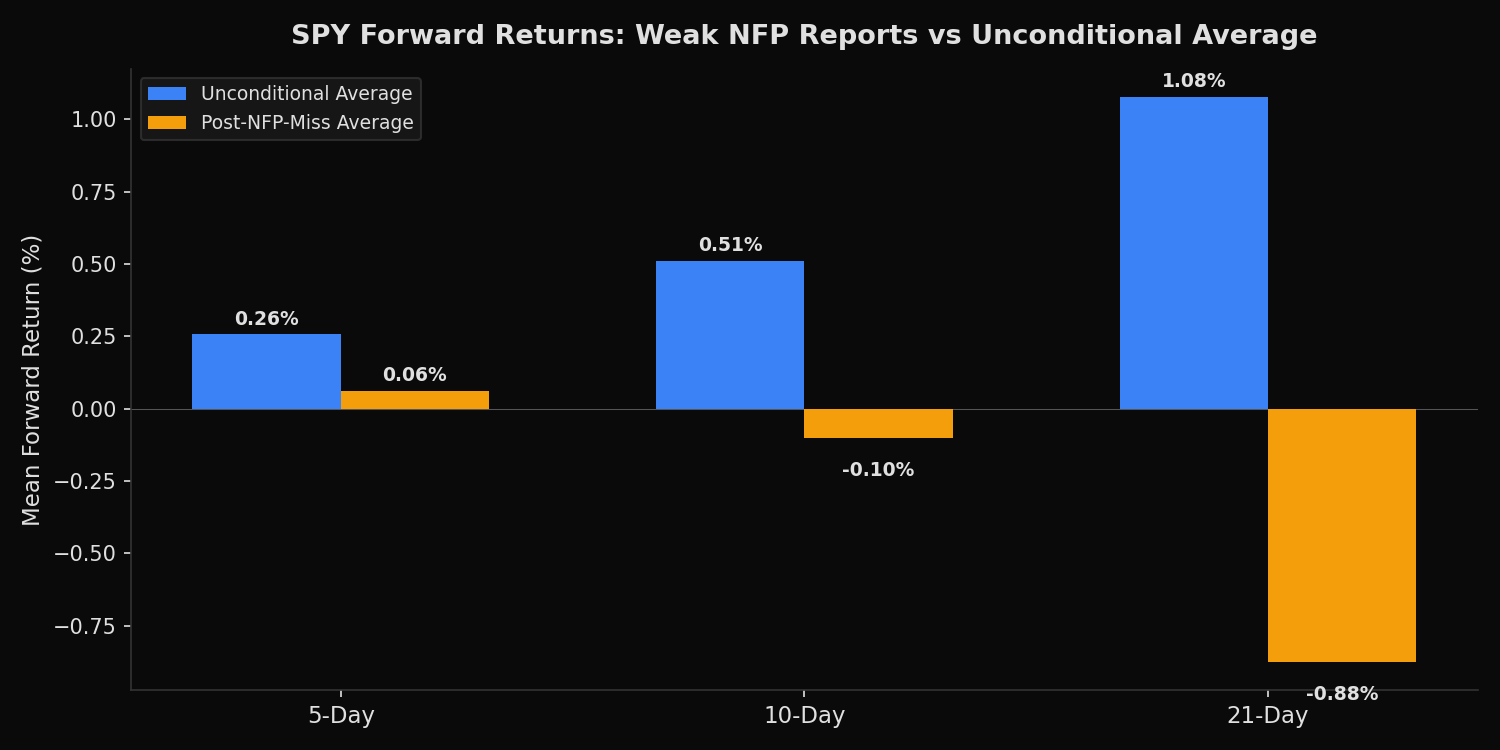

Post-NFP-miss mean: 0.06% -0.10% -0.88%

Unconditional mean: 0.26% 0.51% 1.08%

T-TEST: Post-NFP-miss vs Unconditional

--------------------------------------------------

5-day: t=-0.498, p=0.6365 n=7

10-day: t=-0.722, p=0.4975 n=7

21-day: t=-1.393, p=0.2131 n=7What this tells us

The post-miss average forward return is below the unconditional average at every horizon. At 5 days, the market returns +0.06% after a weak NFP versus +0.26% unconditionally. At 10 days, the gap widens: -0.10% post-miss versus +0.51% unconditional. At 21 days (one trading month), the divergence is most pronounced: -0.88% average post-miss versus +1.08% unconditional. That is a 196 basis point difference.

However, none of these differences are statistically significant. The t-statistics range from -0.50 (5-day) to -1.39 (21-day), and the corresponding p-values range from 0.21 to 0.64. With only 7 observations, the sample is too small to draw definitive conclusions. The standard errors are large relative to the mean differences.

The event-level data reveals substantial dispersion. The September 2021 NFP miss (194K versus 750K expected) preceded a -4.41% drawdown over 21 days. The July 2024 miss (114K) preceded a -6.72% decline. But the February 2019 miss (20K) was followed by a +3.32% rally as the market priced in a Fed pause. The same signal produced opposite outcomes depending on the broader macro context.

The most recent event, July 2026 (57K), does not yet have sufficient forward data. Its inclusion will matter for the trend: if SPY declines from here, the 21-day t-statistic moves closer to significance.

So what?

The directional pattern is clear: weak NFP reports tend to be followed by below-average returns, particularly at the 21-day horizon. The 196 basis point gap between post-miss and unconditional 21-day returns is economically meaningful even if it is not yet statistically significant.

The lack of statistical significance does not mean there is no signal. It means there are not enough observations to confirm the signal with confidence. NFP misses of this magnitude occur roughly once or twice per year. Accumulating a sample large enough for traditional significance (20+ events) would require a decade or more of data, and structural changes in the economy may invalidate older observations.

For practitioners, the implication is to treat weak NFP prints as a risk factor rather than a trading signal. The appropriate response is not to sell the index, but to consider reducing position sizes, tightening stop losses, or hedging tail risk in the 3-4 weeks following a significant payroll miss. The events where the market rallied after a weak report (2016, 2019) both occurred in contexts where the Fed was expected to ease. Events where the market fell (2021, 2024) occurred when inflation was elevated and the Fed had less room to pivot. The macro context determines whether bad news is good news or simply bad news.

Built with xfinlink — free financial data API for Python. pip install xfinlink

pip install xfinlink