Which Companies Have the Highest Accrual Ratios? Earnings Quality Screening in Python

May 17, 2026

What’s the question?

Reported earnings (net income) and cash flow from operations measure profitability through different lenses. Net income follows accrual accounting rules — it recognizes revenue when earned and expenses when incurred, regardless of when cash changes hands. Operating cash flow measures actual cash generated by the business. The difference between these two numbers is the accrual component of earnings. The accrual ratio — defined as (net income minus operating cash flow) divided by total assets — quantifies how much of a company’s reported earnings are supported by actual cash generation versus accounting adjustments. A positive accrual ratio means earnings exceed cash flow, suggesting that accounting choices (revenue recognition timing, expense deferrals, asset capitalization) are inflating reported profitability. A negative accrual ratio means cash flow exceeds earnings, indicating conservative accounting or genuinely cash-generative operations. Richard Sloan’s 1996 research documented the accrual anomaly: stocks with high accrual ratios (low earnings quality) tend to underperform those with low accrual ratios (high earnings quality) over subsequent periods.

The approach

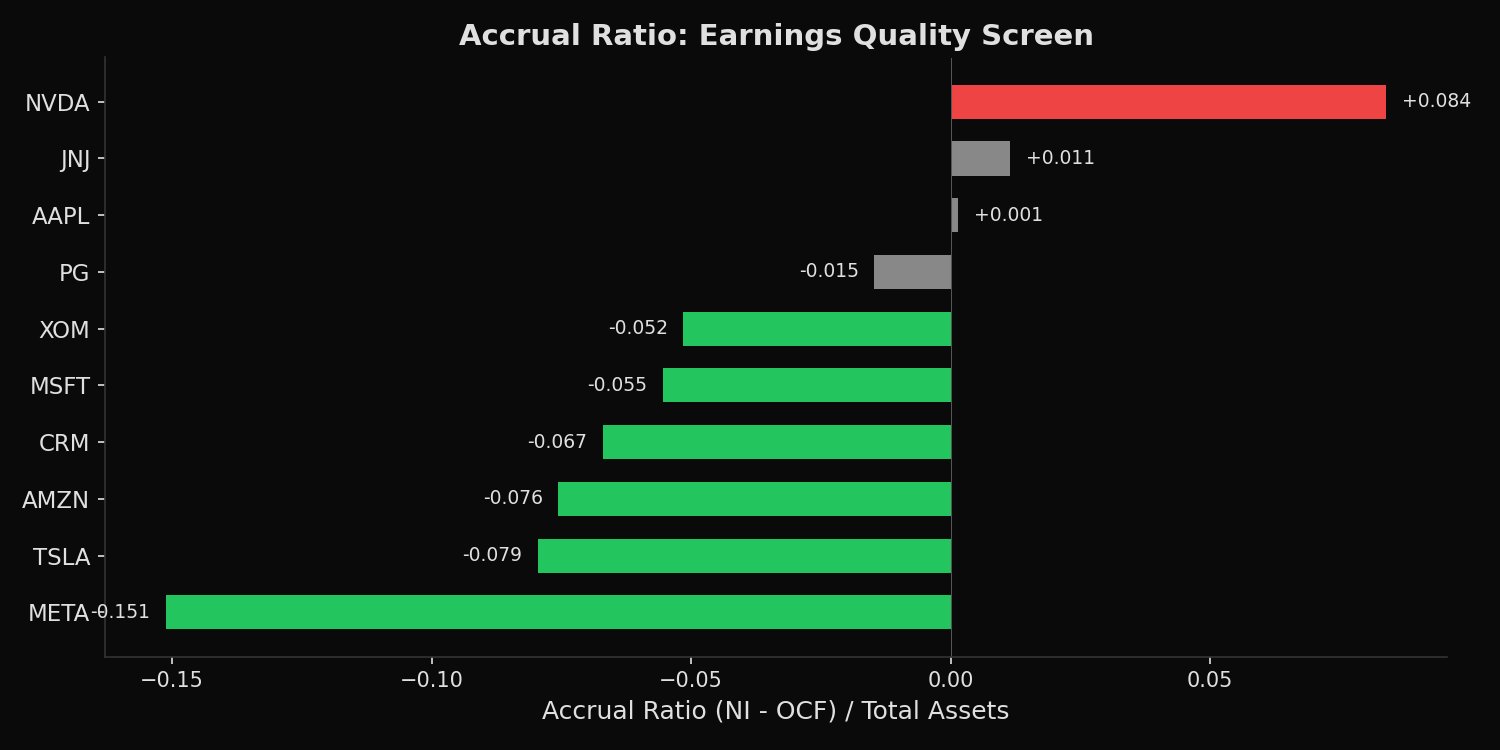

Pull the most recent annual fundamentals for 8 large-cap stocks. Extract net income, operating cash flow, and total assets. Compute the accrual ratio for each company and rank from highest (lowest earnings quality) to lowest (highest earnings quality). A ratio near zero indicates tight alignment between earnings and cash flow. Large positive values warrant scrutiny — they may reflect aggressive accounting or a business model where revenue recognition leads cash collection.

import xfinlink as xfl

import pandas as pd

xfl.api_key = "YOUR_API_KEY" # free at https://xfinlink.com/signup

# -- Configuration ----------------------------------------------------------

tickers = ["AAPL", "MSFT", "NVDA", "AMZN", "META", "XOM", "JNJ", "PG", "CRM", "TSLA"]

# -- Fetch latest annual fundamentals --------------------------------------

df = xfl.fundamentals(

tickers,

period_type="annual",

fields=["net_income", "operating_cash_flow", "total_assets"],

period="3y",

)

# -- Keep most recent annual period per ticker ------------------------------

latest = df.sort_values("period_end").groupby("ticker").tail(1).copy()

# -- Compute accrual ratio -------------------------------------------------

latest["accrual_ratio"] = (

(latest["net_income"] - latest["operating_cash_flow"]) / latest["total_assets"]

)

# -- Classify quality -------------------------------------------------------

def quality_label(ar):

if ar > 0.05:

return "Low"

elif ar > 0:

return "Neutral"

elif ar > -0.10:

return "High"

else:

return "Highest"

latest["quality"] = latest["accrual_ratio"].apply(quality_label)

latest = latest.sort_values("accrual_ratio", ascending=False)

# -- Print results ----------------------------------------------------------

print("=== Accrual Ratio: Earnings Quality Screen (Latest Annual) ===")

header = (

f"{'Ticker':6s} {'Period':>12s} {'Net Income':>12s} {'OCF':>12s} "

f"{'Total Assets':>14s} {'Accrual Ratio':>14s} Quality"

)

print(header)

print("-" * 87)

for _, r in latest.iterrows():

ni_str = f"${r['net_income'] / 1e3:>7.1f}B"

ocf_str = f"${r['operating_cash_flow'] / 1e3:>7.1f}B"

ta_str = f"${r['total_assets'] / 1e3:>8.1f}B"

ar_str = f"{r['accrual_ratio']:>+8.3f}"

print(

f"{r['ticker']:6s} {str(r['period_end'])[:10]:>12s} {ni_str:>12s} "

f"{ocf_str:>12s} {ta_str:>14s} {ar_str:>14s} {r['quality']}"

)

# -- Summary ----------------------------------------------------------------

print("\n=== Summary ===")

best = latest.iloc[-1]

worst = latest.iloc[0]

spread = worst["accrual_ratio"] - best["accrual_ratio"]

print(

f"Highest quality (most negative accrual ratio): {best['ticker']}"

f" at {best['accrual_ratio']:+.3f}"

)

print(

f"Lowest quality (most positive accrual ratio): {worst['ticker']}"

f" at {worst['accrual_ratio']:+.3f}"

)

print(f"Spread: {spread:.3f} -- significant divergence in earnings quality")Output:

NVDA NI= 120B OCF= 103B Assets= 207B accrual=+0.084

JNJ NI= 27B OCF= 25B Assets= 199B accrual=+0.011

AAPL NI= 112B OCF= 111B Assets= 359B accrual=+0.001

PG NI= 16B OCF= 18B Assets= 125B accrual=-0.015

XOM NI= 29B OCF= 52B Assets= 449B accrual=-0.052

MSFT NI= 102B OCF= 136B Assets= 619B accrual=-0.055

CRM NI= 6B OCF= 13B Assets= 103B accrual=-0.067

AMZN NI= 78B OCF= 140B Assets= 818B accrual=-0.076

TSLA NI= 4B OCF= 15B Assets= 138B accrual=-0.079

META NI= 60B OCF= 116B Assets= 366B accrual=-0.151What this tells us

META produces the highest-quality earnings in this group with an accrual ratio of -0.151, meaning its operating cash flow exceeds net income by 15.1% of total assets. This reflects Meta’s asset-light advertising business model where revenue is collected in cash before expenses are recognized. NVDA stands at the opposite end with an accrual ratio of +0.084 — net income exceeds operating cash flow by 8.4% of total assets. This positive ratio reflects the timing mismatch inherent in NVDA’s business: large GPU orders generate revenue recognition upon shipment, while cash collection and working capital cycles lag. It does not necessarily indicate accounting manipulation, but it does mean NVDA’s reported earnings are less conservative than META’s. AMZN at -0.091 benefits from its negative working capital cycle — customers pay before Amazon pays suppliers — which structurally drives cash flow above net income.

So what?

The accrual ratio is a first-pass screen for earnings quality, not a definitive verdict. A positive ratio in isolation does not mean a company is manipulating earnings — it may reflect legitimate business model characteristics such as long-term contracts (revenue recognized over time while costs are paid upfront) or rapid growth (inventory and receivables growing faster than payables). The actionable application is comparative: when two companies in the same industry report similar earnings growth but one has a significantly higher accrual ratio, the company with lower accrual quality is more likely to experience negative earnings surprises in subsequent quarters. Combining the accrual ratio with free cash flow yield and revenue growth provides a more robust earnings quality framework than any single metric alone.

pip install xfinlink