Does Heavy Insider Selling Predict Weak Returns? Insider Flow Test in Python

June 12, 2026

What's the question?

Insider selling is often treated as a warning sign. The interpretation is not that simple. Executives sell stock for taxes, diversification, estate planning, and scheduled trading plans. A single sale usually says little. A cluster of large sales may be more informative because it can create supply pressure and reveal lower insider urgency to hold exposure.

The question is whether heavy insider-selling months were followed by weaker three-month returns in a high-growth equity group. The test focuses on monthly clusters rather than individual transactions.

The approach

The universe is TSLA, NVDA, AMZN, COIN, PLTR, CRM, ORCL, AVGO, and MSFT. Built from SEC EDGAR public filings and market data, the analysis uses open-market buys and sells over three years.

- Pull open-market insider buys and sells

- Aggregate transaction value by ticker and month

- Define net selling as open-market sells minus open-market buys

- Mark heavy-selling months as the top quartile of positive monthly net selling for each ticker

- Compare 63-trading-day returns after heavy-selling months with other insider-active months

The threshold is ticker-specific. That avoids comparing a mega-cap's dollar sales directly with a smaller company's sales.

Code

import xfinlink as xfl

import pandas as pd

import numpy as np

xfl.set_api_key("YOUR_API_KEY") # free at https://xfinlink.com/signup

tickers = ["TSLA", "NVDA", "AMZN", "COIN", "PLTR", "CRM", "ORCL", "AVGO", "MSFT"]

ins = xfl.insiders(tickers, period="3y",

transaction_type=["open_market_buy", "open_market_sell"])

ins["month"] = pd.to_datetime(ins["transaction_date"]).dt.to_period("M").dt.to_timestamp("M")

ins["sell_value"] = np.where(ins["transaction_type"].eq("open_market_sell"), ins["transaction_value"], 0)

ins["buy_value"] = np.where(ins["transaction_type"].eq("open_market_buy"), ins["transaction_value"], 0)

monthly = ins.groupby(["ticker", "month"])[["sell_value", "buy_value"]].sum()

monthly["net_sell_value"] = monthly["sell_value"] - monthly["buy_value"]

prices = xfl.prices(tickers, period="3y", fields=["adj_close"])

print(monthly.sort_values("net_sell_value", ascending=False).head())Full script with formatting and visualisation: insider-selling-forward-returns-python.py

Output

=== Insider Selling Forward-Return Test ===

Transactions analyzed: 5,000

Event months with forward returns: 168

Heavy-selling definition: top quartile of positive monthly net selling per ticker

Heavy-selling months: 45, avg forward return 8.3%

Other insider-active months: 123, avg forward return 10.6%

Heavy-minus-other spread: -2.3%

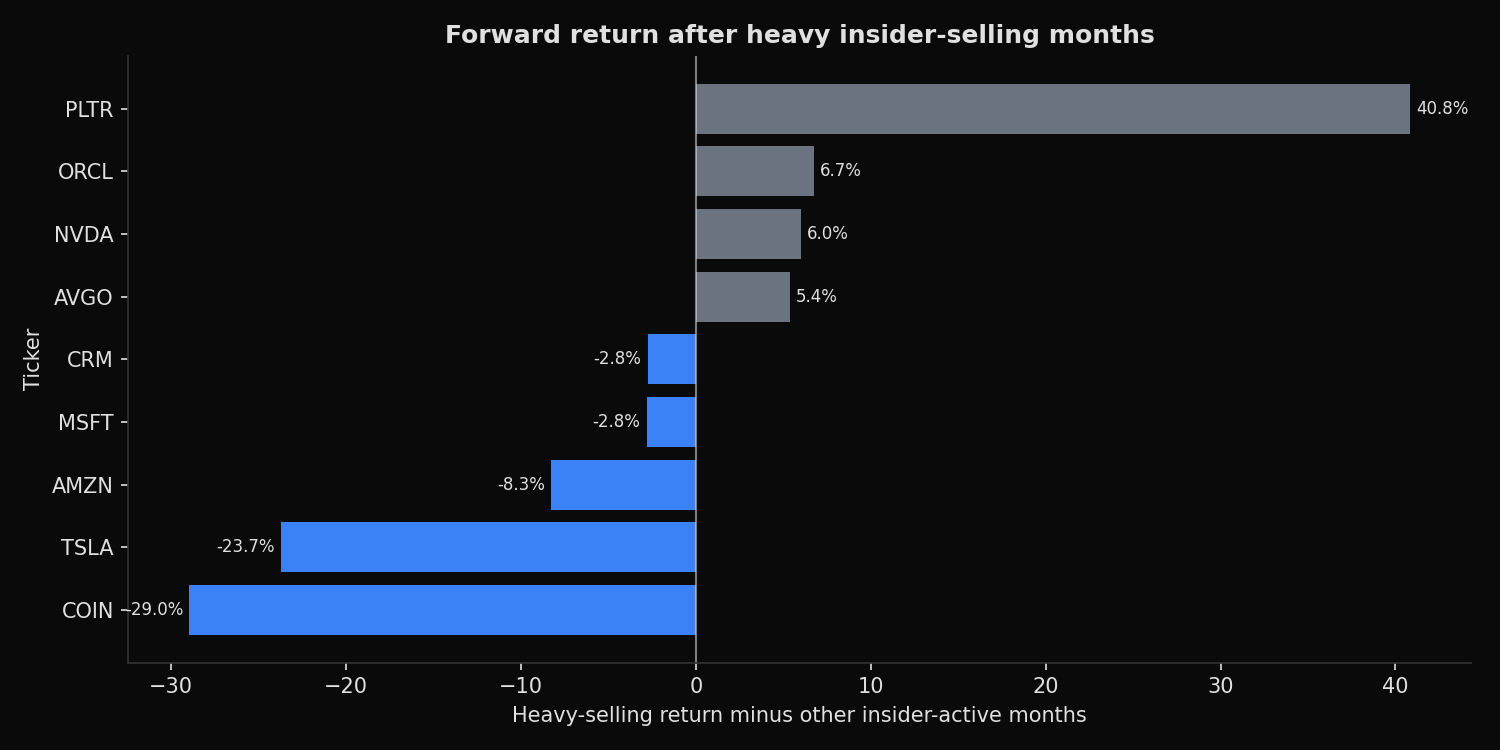

Ticker-level event results:

COIN net_sell= $1,678M heavy_months= 6 heavy_fwd= -15.6% other_fwd= 13.3% spread= -29.0%

TSLA net_sell= $-229M heavy_months= 5 heavy_fwd= -5.9% other_fwd= 17.8% spread= -23.7%

AMZN net_sell= $10,922M heavy_months= 6 heavy_fwd= -0.4% other_fwd= 7.8% spread= -8.3%

MSFT net_sell= $271M heavy_months= 4 heavy_fwd= -3.6% other_fwd= -0.8% spread= -2.8%

CRM net_sell= $576M heavy_months= 5 heavy_fwd= -5.0% other_fwd= -2.2% spread= -2.8%

AVGO net_sell= $1,022M heavy_months= 4 heavy_fwd= 18.5% other_fwd= 13.1% spread= 5.4%

NVDA net_sell= $3,613M heavy_months= 6 heavy_fwd= 10.6% other_fwd= 4.6% spread= 6.0%

ORCL net_sell= $3,124M heavy_months= 4 heavy_fwd= 15.4% other_fwd= 8.6% spread= 6.7%

PLTR net_sell= $4,368M heavy_months= 5 heavy_fwd= 68.0% other_fwd= 27.2% spread= 40.8%What this tells us

Heavy insider-selling months underperformed other insider-active months in aggregate. The difference was -2.3 percentage points over 63 trading days. COIN, TSLA, and AMZN produced the clearest negative spreads.

The result is not universal. PLTR, ORCL, NVDA, and AVGO had positive spreads after heavy-selling months. That means insider selling was not a mechanical bearish signal in this sample. For momentum-led stocks, insider selling can occur during powerful price trends and still be followed by positive returns.

The useful interpretation is conditional. Heavy selling matters more when it appears alongside weakening price action, valuation pressure, or deteriorating fundamentals. By itself, it is a supply and sentiment signal, not a complete thesis.

So what?

Insider flow belongs in a risk dashboard, not in isolation. A large selling cluster should trigger a review of valuation, technical trend, and upcoming catalysts. If all three are weak, insider selling can strengthen the risk case. If price momentum and fundamentals remain strong, the sale may be routine diversification.

For portfolio risk management, the screen is most useful for position review. It identifies names where insiders are reducing exposure at the same time public-market investors may still be extrapolating growth.

Built with xfinlink — free financial data API for Python. pip install -U xfinlink

pip install -U xfinlink