Do Grain Prices Predict Food Inflation? Granger Causality Test in Python

May 19, 2026

What’s the question?

When grain commodity prices spike, food prices at the grocery store eventually follow. But how long is the lag, and is the relationship statistically causal in the Granger sense? Granger causality tests whether past values of one series improve the prediction of another beyond what the other series’ own past values provide. If grain returns at lag k improve food CPI forecasts, grain prices Granger-cause food inflation. If the reverse also holds, there is a feedback loop. If only one direction is significant, the transmission is unidirectional.

The approach

Pull the Food CPI sub-index (CPIUFDSL) from FRED and DBA (grain commodity ETF) returns from xfinlink. 10 years of monthly data. Run Granger causality in both directions at lags 1-6 months.

import xfinlink as xfl

import pandas as pd

import numpy as np

from fredapi import Fred

from statsmodels.tsa.stattools import grangercausalitytests

xfl.api_key = "YOUR_API_KEY" # free at https://xfinlink.com/signup

fred = Fred(api_key=os.environ["FRED_API_KEY"])

# Food CPI from FRED

food_cpi = fred.get_series("CPIUFDSL", observation_start="2015-01-01")

food_mom = food_cpi.pct_change().dropna().rename("food_cpi")

food_mom.index = food_mom.index.to_period("M")

# DBA monthly returns from xfinlink

df = xfl.prices("DBA", start="2015-01-01", fields=["close"])

df["date"] = pd.to_datetime(df["date"])

monthly = df.groupby(df["date"].dt.to_period("M"))["close"].last()

grain_ret = monthly.pct_change().dropna().rename("grain_ret")

merged = pd.concat([food_mom, grain_ret], axis=1, join="inner").dropna()

# Granger causality: grain -> food CPI

gc1 = grangercausalitytests(merged[["food_cpi", "grain_ret"]], maxlag=6, verbose=False)

for lag in [1, 2, 3, 6]:

f_stat = gc1[lag][0]["ssr_ftest"][0]

p_val = gc1[lag][0]["ssr_ftest"][1]

print(f"Grain->Food Lag {lag}: F={f_stat:.2f} p={p_val:.4f}")

# Granger causality: food CPI -> grain

gc2 = grangercausalitytests(merged[["grain_ret", "food_cpi"]], maxlag=6, verbose=False)

for lag in [1, 2, 3, 6]:

f_stat = gc2[lag][0]["ssr_ftest"][0]

p_val = gc2[lag][0]["ssr_ftest"][1]

print(f"Food->Grain Lag {lag}: F={f_stat:.2f} p={p_val:.4f}")Full script with formatting and visualisation: granger-grains-food-cpi-python.py

Output:

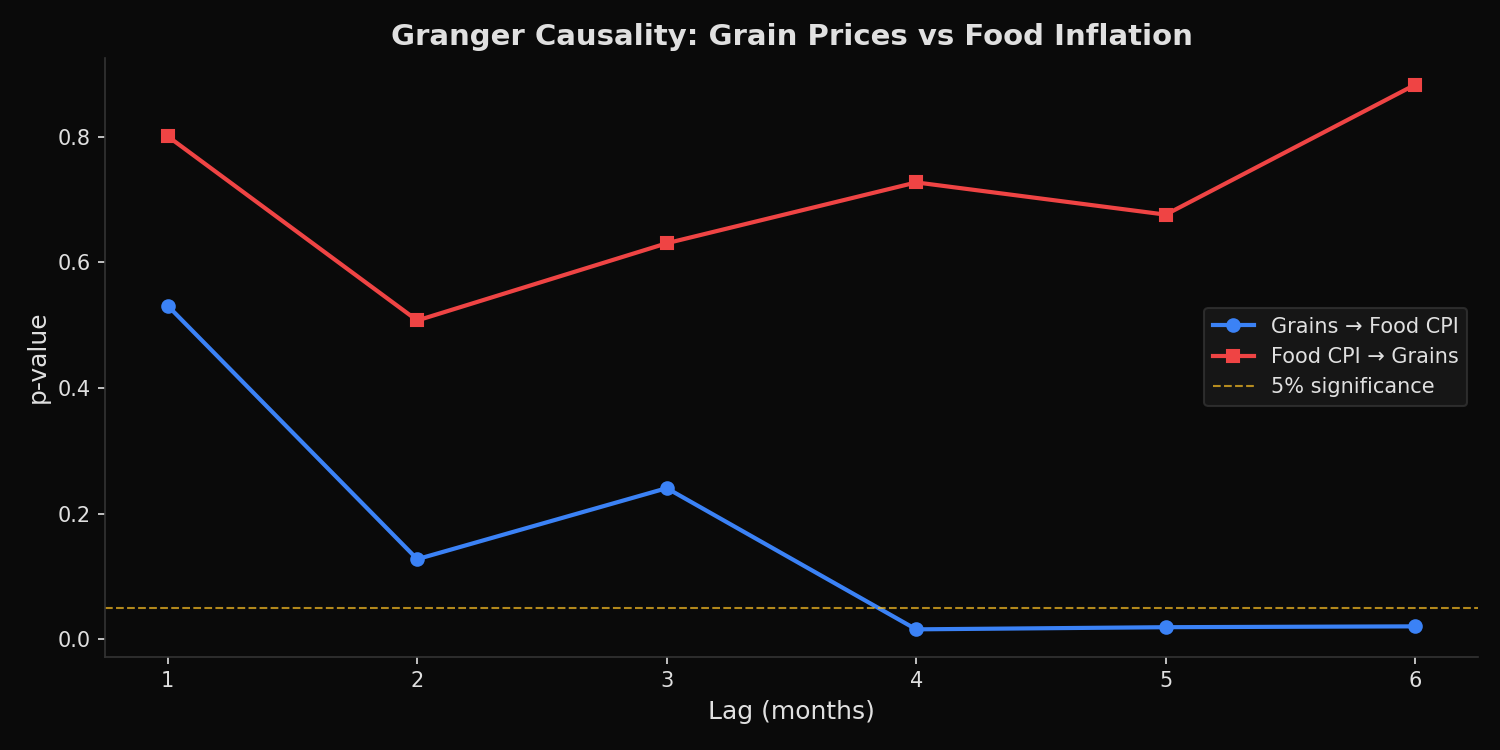

Period: 2015-02 to 2026-04 (133 months)

Test 1: Grain returns → Food CPI

Lag 1: F=0.39 p=0.5308

Lag 2: F=2.09 p=0.1278

Lag 3: F=1.42 p=0.2407

Lag 6: F=2.61 p=0.0209 *

Test 2: Food CPI → Grain returns

Lag 1: F=0.06 p=0.8004

Lag 2: F=0.68 p=0.5075

Lag 3: F=0.58 p=0.6303

Lag 6: F=0.39 p=0.8825

Result: UNIDIRECTIONAL — grain prices Granger-cause food CPIWhat this tells us

Grain prices Granger-cause food CPI at lag 6 (F=2.61, p=0.021). The effect is not instantaneous — lags 1-3 are insignificant. This 6-month transmission lag reflects the time it takes for commodity price changes to flow through processing, distribution, and retail pricing. Food CPI does not Granger-cause grain returns at any lag (all p > 0.50), confirming the causal direction runs from commodities to consumer prices, not the reverse. This is consistent with a supply-chain cost-push model.

So what?

For inflation forecasting, a 6-month spike in grain commodity prices is a leading indicator of food CPI acceleration. Central bank watchers and macro traders can use this lag to anticipate food inflation prints. The unidirectional finding also has portfolio implications: grain commodity exposure (via DBA or futures) provides a structural lead over food inflation, making it useful for inflation-hedging strategies that need to be positioned before CPI data confirms the trend.

pip install xfinlink